The end of Medicaid continuous enrollment March 31, 2023, means an estimated 15 million Americans could lose Medicaid and need health insurance — and that’s just one of several converging factors creating an unprecedented opportunity for insurance agents.

The so-called “family glitch” and the 2019 creation of the individual coverage health reimbursement account (ICHRA) are combining with the end of Medicaid continuous enrollment to drive millions of consumers into the under-65 individual health insurance space, including the Affordable Care Act (ACA) Marketplace.

![]() While Senior Market Sales® (SMS) has been a leader in the Medicare health insurance market for four decades, its acquisition of O’Neill Marketing marks its entry into the under-65 individual health insurance market, allowing SMS-contracted agents access to O’Neill Marketing’s robust ACA product and technology platform.

While Senior Market Sales® (SMS) has been a leader in the Medicare health insurance market for four decades, its acquisition of O’Neill Marketing marks its entry into the under-65 individual health insurance market, allowing SMS-contracted agents access to O’Neill Marketing’s robust ACA product and technology platform.

“Just as agents have relied on SMS for Medicare sales, we are now positioned to offer the same high-quality support to get agents up and running in time for this wave needing individual health insurance coverage,” said SMS President Jim Summers. “The timing could not be better for agents to enter the under-65 health market, and now SMS is positioned to support agents with the tools and resources from an established leader in that space.”

While entering the under-65 market can be a smart move for the long-term, helping with the immediate coverage crisis requires quick action because of the massive need and upcoming enrollment deadlines.

The Centers for Medicare and Medicaid Services (CMS) called the end of Medicaid continuous enrollment the “single largest health coverage transition event since the first Marketplace Open Enrollment following enactment of the (ACA).” A Marketplace special enrollment period (SEP) for people who are unenrolled from Medicaid coverage started March 31, 2023, and runs through July 31, 2024. This SEP, called the “Unwinding SEP,” gives individuals who lose Medicaid up to 60 days to enroll after losing coverage.

To learn more, read on. Contact SMS to learn more about getting into the ACA market.

Understanding the ACA Opportunity

Understanding the ACA Opportunity

The ACA, often referred to as Obamacare, was enacted in March 2010 as comprehensive health care reform designed to do three main things:

- Make affordable health insurance available to more Americans by providing new premium tax credits for the purchase of private health insurance

- Expand Medicaid, the government-run health coverage for people with limited incomes

- Support innovative medical care delivery methods to lower health care costs

To achieve these goals, the law established the Health Insurance Marketplace, often called the Marketplace or exchange for short, as the platform for individuals, families and small businesses to purchase private health insurance. In most states, the federal government runs the Marketplace, at HealthCare.gov, but some states run their own Marketplaces at different websites.

Some people who apply for coverage through the Marketplace may qualify for coverage through Medicaid or the Children’s Health Insurance Program (CHIP), which are free or low-cost health programs. If they do qualify, their state will enroll them. (The ACA requires states to coordinate eligibility and enrollment processes between Medicaid, state CHIPs and subsidized coverage on health insurance exchanges.)

How Medicaid Factors Into the ACA

The expansion of Medicaid wasa major cornerstone of the ACA, but also a major point of controversy and confusion.

The ACA expanded Medicaid eligibility to adults with incomes up to 138% of the federal poverty level and provided states with an enhanced federal matching rate for their expansion populations. Medicaid expansion originally was a requirement. But the U.S. Supreme Court ruled in 2012 that states can opt out of it.

The result: moststates expanded their Medicaid programsto cover all people with household incomes below a certain level, while others haven’t.

What is Medicaid Redetermination?

Before the COVID-19 pandemic, Medicaid recipients had to renew coverage every year to keep getting benefits — a process called “redetermination,” in which the states review eligibility. Policies that affect individuals’ ability to maintain Medicaid coverage vary by state.

But early in the pandemic, Congress enacted the Families First Coronavirus Response Act (FFCRA), which required states to keep people enrolled in Medicaid throughout the COVID-19 public health emergency as a condition of receiving a temporary increase in the federal share of Medicaid costs. As part of the Consolidated Appropriations Act of 2023, Congress set an end of March 31, 2023, for the continuous enrollment provision. That means states that accept the enhanced federal funding could resume Medicaid disenrollments beginning in April 2023.

But early in the pandemic, Congress enacted the Families First Coronavirus Response Act (FFCRA), which required states to keep people enrolled in Medicaid throughout the COVID-19 public health emergency as a condition of receiving a temporary increase in the federal share of Medicaid costs. As part of the Consolidated Appropriations Act of 2023, Congress set an end of March 31, 2023, for the continuous enrollment provision. That means states that accept the enhanced federal funding could resume Medicaid disenrollments beginning in April 2023.

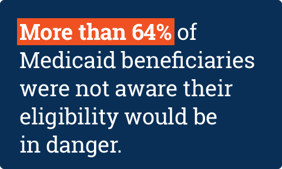

The redeterminations of tens of millions of beneficiaries require states to do in a matter of months what they previously would have been doing continuously over multiple years. Beneficiaries who enrolled in Medicaid during the pandemic may be unaware of the need to renew now because they were never exposed to the normal Medicaid renewal process. A December 2022 survey published by the Robert Wood Johnson Foundation revealed that more than 64% of Medicaid beneficiaries surveyed were not aware their eligibility for Medicaid could be in danger.

How Many Could Lose Medicaid Coverage?

The need for Medicaid surged during the pandemic because of economic hardships such as job loss. Consequently, Medicaid enrollment grew substantially during the pandemic compared to before the pandemic, primarily due to the continuous enrollment provision. A KFF analysis estimates that enrollment in Medicaid and CHIP will have grown by 23.3 million enrollees, to nearly 95 million, by the end of March 2023.

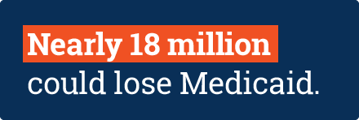

The number expected to lose coverage during the unwinding process varies but is in the millions. While the federal government projects the total number of individuals to be disenrolled to be 15 million, KFF estimates between 5 and 14 million could lose their Medicaid coverage, and the Urban Institute estimates nearly 18 million could lose Medicaid.

The number expected to lose coverage during the unwinding process varies but is in the millions. While the federal government projects the total number of individuals to be disenrolled to be 15 million, KFF estimates between 5 and 14 million could lose their Medicaid coverage, and the Urban Institute estimates nearly 18 million could lose Medicaid.

Those losing Medicaid health coverage also are at risk of losing another critical coverage. New data released by CareQuest Institute for Oral Health reveals tha more than 14 million adults may lose dental coverage under the Medicaid redetermination process. (SMS can help you connect clients to affordable dental plans from top carriers.)

The Medicaid Coverage Gap

Nearly 400,000 working-age adults will lose insurance because they fall into the Medicaid coverage gap — that is, they live in states that have not yet expanded Medicaid eligibility, according to theCommonwealth Fund.

Adults who fall into this coverage gap — not to be confused with Medicare Part D coverage gaps — have incomes above their state’s eligibility threshold for Medicaid but below the minimum income eligibility for tax credits through the ACA marketplace. (The ACA’s premium tax credits, or subsidies, lower costs for households with incomes between 100% and 400% of the federal poverty level.) Because the original ACA envisioned that all people with incomes below the federal poverty level would be eligible for Medicaid, there was no need identified for ACA marketplace eligibility below the poverty level.

Insurance agents in the under-65 market can play an important role in helping people in the Medicaid coverage gap, as well as people who buy individual health insurance plans outside the Marketplace.

How ACA Marketplace Subsidies Work

To receive thetwo types of government subsidies, qualifying individuals must enroll in a plan offered through a health insurance marketplace. (People can also buy individual health plans outside of the Marketplace — for example, if they think they won’t qualify for financial assistance.)

The importance of subsidies is evidenced in enrollment numbers. The individual health insurance market grew rapidly in the ACA’s early years, but the gains were partially offset by subsequent declines, particularly among people not receiving subsidies amid steep premium increases, according toKFF.

The importance of subsidies is evidenced in enrollment numbers. The individual health insurance market grew rapidly in the ACA’s early years, but the gains were partially offset by subsequent declines, particularly among people not receiving subsidies amid steep premium increases, according toKFF.

Subsidies provided through theAmerican Rescue Plan Act(ARPA) in 2021 helped reverse the declining trend, because under the new law:

- More people than ever before qualify for help paying for health coverage — even those who weren’t eligible in the past

- Most people currently enrolled in Marketplace plans may qualify for more tax credits

- Health insurance premiums after these new savings will go down

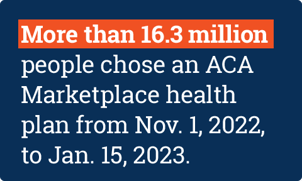

These factors helped contribute to a record-high enrollment —more than 16.3 million peoplechose an ACA Marketplace health plan during the most recent open enrollment period — Nov. 1, 2022, to Jan. 15, 2023 — the largest enrollment since the ACA started providing subsidized health insurance in 2014.

In 2022, Congress extended the subsidies for three years, through 2025, with the passage of theInflation Reduction Act. Several states also have provided subsidies to individuals purchasing Marketplace plans.

The extension of subsidies will play an important role in allowing people to maintain or attain affordable health insurance, but additional subsidies aren’t the only means toward this end. This past open enrollment season saw a rule change designed to help families — the infamous “family glitch” was fixed.

What Is the Family Glitch?

Until 2023, people with an offer of “affordable” job-based coverage, such as through a family member’s job, were generally ineligible for Marketplace subsidies. However, the definition of “affordable” was not feasible for many. This so-called family glitch left5.1 million people ineligiblefor marketplace subsidies until it was fixed for the 2023 coverage year.

New federal regulations published in fall 2022 changedthe way “affordable” job-based coverage is determined. Previously, regulations based eligibility for a family’s premium subsidies on whether the employer-sponsored insurance was affordable for employee-only coverage. The often-substantial additional premium to cover family members was not considered. Under the new federal regulations, however, the worker’s required premium contributions for self-only coverage and for family coverage were compared to the affordability threshold of 9.12% of household income.

New federal regulations published in fall 2022 changedthe way “affordable” job-based coverage is determined. Previously, regulations based eligibility for a family’s premium subsidies on whether the employer-sponsored insurance was affordable for employee-only coverage. The often-substantial additional premium to cover family members was not considered. Under the new federal regulations, however, the worker’s required premium contributions for self-only coverage and for family coverage were compared to the affordability threshold of 9.12% of household income.

This fix of the family glitch meant that some consumers with access to employer-sponsored family coverage with high premiums were able for the first time to enroll in Marketplace plans with subsidies that might make family coverage more affordable to them.

In addition to the opportunity that the fix presents for insurance agents helping families, it also will help employers connect employees with more affordable plans. In this way, SMS’ acquisition of O’Neill Marketing helps expand the reach ofAlliant Insurance Services, whichacquired SMS in 2020. Alliant, one of the nation’s largest and fastest-growing insurance brokerage and consulting firms, can now offer employers the ability to help employees with non-covered spouses and children attain ACA coverage.

Employers and employees also gained more choices in health care coverage when a federal rule allowing for use ofindividual coverage health reimbursement arrangements(ICHRAs) was implemented in January 2020.

What Is ICHRA?

Under the new rule, businesses can meet ACA coverage requirements by reimbursing employees for health insurance of their choice on a tax-free basis, rather than providing an employer-sponsored group health plan.

With ICHRAs, the employer chooses a fixed-dollar amount to be available for employee reimbursement, and the employees choose and purchase their own qualifying health insurance plan from the open market to be submitted for employer reimbursement. ICHRAs give employees a broader range of options than an employer’s group plan offerings — typically one or two plans from one insurer — while giving businesses theability to cap financial exposureto rising health insurance costs and ease some of the administrative hassle that comes with traditional plans.

By partnering with O’Neill Marketing, SMS-contracted agents now have access to support so they can enter this new market of ICHRA employees unleashed from group plans into the open market, as well as those employees from small businesses, which are increasingly adopting ICHRAs.

A Growing ICHRA Market

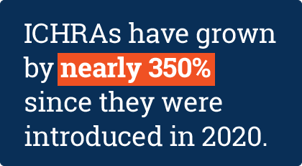

ICHRAs have grown by nearly 350% since they were introduced in 2020 amidst market growth for all HRAs, according to theHRA Council 2022 Growth Trends Report.

While large employers represent the fastest growing segment of businesses adopting this strategy, ICHRAs are promising for small businesses, which have struggled to provide health benefits to employees because of the high cost and administrative burdens, according to the report. Among small employers — those with fewer than 50 employees and not required to offer coverage — 80% of employers offering ICHRA and a similar type of plan called aqualified small employer health reimbursement arrangement(QSEHRAs) areoffering benefits for the first time.

While large employers represent the fastest growing segment of businesses adopting this strategy, ICHRAs are promising for small businesses, which have struggled to provide health benefits to employees because of the high cost and administrative burdens, according to the report. Among small employers — those with fewer than 50 employees and not required to offer coverage — 80% of employers offering ICHRA and a similar type of plan called aqualified small employer health reimbursement arrangement(QSEHRAs) areoffering benefits for the first time.

Also fueling ICHRA popularity is itsability to extend benefits to traditionally difficult-to-insure groupssuch as part-time and seasonal workers, segments that have grown in the wake of the pandemic. Employers can offer ICHRAs to certain types of employees, based on certain job-based criteria — such as full-time or part-time status or coverage by a collective bargaining agreement — but employers can’t make up their own classes.

The federal government has estimated that by the time employers have fully adjusted to the rule,800,000 previously uninsured peoplemay get access to health insurance as a result.

Insurance agents in the under-65 individual health insurance market will be positioned to benefit from the increased popularity of ICHRAs.

How to Enter the Under-65 Individual Health Insurance Market

Agents wanting to enter the under-65 market can leverage O’Neill Marketing’s expertise and technology, along with its ancillary products available for add-on sales — all reasons SMS acquired the St. Petersburg, Florida, company, Summers said.

Charles (Chuck) O’Neill, who foundedO’Neill Marketingin 2016, grew the general agency with Kerry Van Iseghem leading the organization as Chief Executive Officer into a leading distributor in the ACA market with products from more than 100 health carriers. In 2022, the agency’s 1,500 agents nationwide were responsible for more than 100,000 ACA enrollments.

O’Neill Marketing’s heavy investment in technology includes a proprietary agent portal and quoting and enrollment tools that help them do business at scale. SMS agents gain access to not only those tools but also agent empowerment and marketing resources and back-office support for all their ACA business.

“As the ACA market continues to grow, there needs to be a tectonic shift in the industry toward technology and efficiencies,” said O’Neill, President and Founder. “If you’re not understanding, accepting and embracing technology, I think the world's going to pass you by, because companies like us are coming.”

While other companies approached O’Neill Marketing to acquire it, the executives chose SMS for its ability to quickly deliver the ACA technology to agents, Van Iseghem said.

“This is going to give us an opportunity to become one of the largest ACA agencies in the country,” he said.

To learn more about the opportunity and how SMS can help,fill out this formor call 1.800.786.5566 to speak with a marketing consultant.

Share this blog post: